Men want to smell good now.

CPG and retail news from the week of 10/13/25

Hello hello!

Influencer marketing is getting expensive. Beyond the partnerships themselves, the tools necessary to source, gift, and create affiliates + contracts add up so quickly.

That’s why we’re so excited to partner with the folks at Endlss, the influencer platform that lets you use all of its features… for FREE. Endlss makes every dollar count with…

A free tier that’s ACTUALLY useful, giving you access to its full tooling

Pricing scales with you—at half the price of other solutions!!!

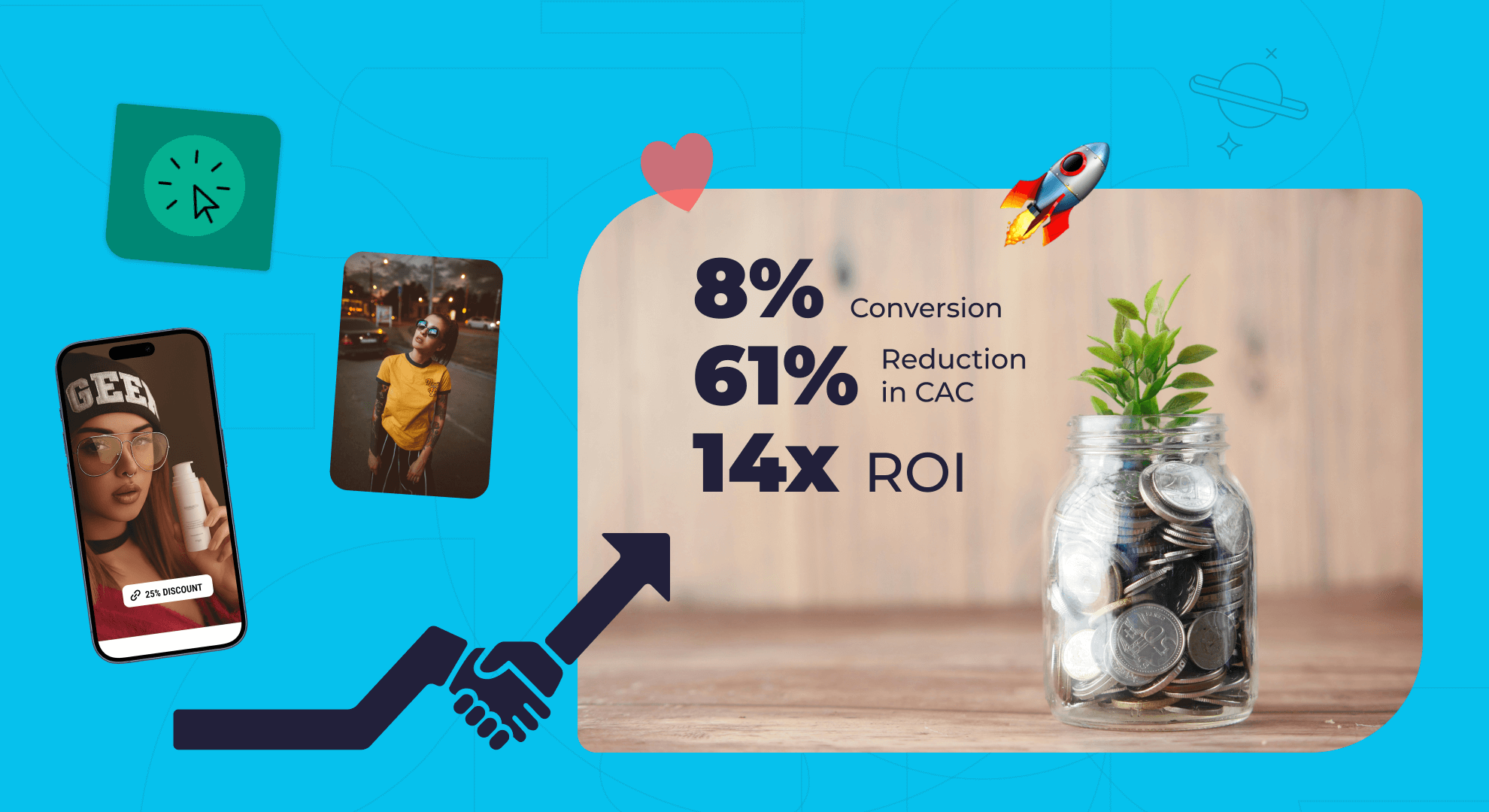

Real numbers: 5¢ CPC, 61% CAC reduction, 14x ROI

With Endlss, you can discover the best influencers for your brand, manage UGC agreements, issue smart affiliate links, and so much more... all in one platform.

Make every influencer dollar count. 👇

Now, let’s get into the news of the week →